Shepherd Outsourcing opened its doors in 2021, and has been providing great services to the ARM industry ever since.

About

Address

©2024 by Shepherd Outsourcing.

Managing several debts at once can feel overwhelming, not to mention expensive. The stress of tracking due dates, juggling payments, and watching balances barely move can take a serious toll on your finances and peace of mind.

Many people turn to debt consolidation as a way to simplify their monthly obligations. In fact, a September 2023 survey by Forbes Advisor found that among 1,000 individuals who used personal loans for debt consolidation, over half did so to simplify and reduce their payments, 54% aimed to secure lower interest rates, and 42% wanted to reduce their overall debt burden.

Debt consolidation can sound like a smart solution. But is it the right move for your situation? In this post, you’ll learn exactly how debt consolidation works, its potential benefits and drawbacks, who it typically helps, and what other options might make more sense if it doesn’t.

Debt consolidation means combining multiple debts into a single loan with one monthly payment—ideally at a lower interest rate. It’s a strategy that helps simplify repayment and may reduce the total amount you pay over time.

For example, if you’re juggling three credit card balances, you could take out a personal loan to pay them off and replace them with one fixed monthly payment. Common forms of debt that people consolidate include credit cards, personal loans, and medical bills.

The loan consolidation definition typically refers to using a new loan to repay several existing debts, streamlining your finances and potentially lowering your costs.

To get a better idea, we suggest you explore our blog, The Truth About Debt Consolidation Loans: Facts vs. Myths.

Debt consolidation works by combining multiple debts into a single, streamlined payment—ideally with better terms. Instead of juggling several due dates and interest rates, you make just one monthly payment to a new lender or account.

This process typically involves taking out a new loan or opening a new credit account to pay off your existing debts. You’ll still owe the same total amount, but with the right terms—such as a lower interest rate or longer repayment period—you could reduce monthly pressure and potentially save money over time.

Keep in mind:

If used responsibly, this method can offer a fresh financial start, but it’s important to commit to the repayment plan.

Next, let’s look at the different types available to help you choose the best fit for your situation.

There are a few common ways to do this, each with its own pros, risks, and ideal use cases. The best way to consolidate your debt varies depending on your financial profile. Below are the methods used for debt consolidation:

This is a personal loan you take out to pay off multiple debts—like three credit cards, a medical bill, and a personal loan—all at once. You’re left with one fixed monthly payment, often at a lower interest rate. If you have a good credit score, this can be an efficient and predictable way to regain control.

A balance transfer card offers a 0% introductory APR for a set period—usually between 12 and 21 months. You move your high-interest credit card balances onto this card and aim to pay it off within the promo period. It’s ideal if your debt is entirely from credit cards and you’re confident you can stick to a payoff plan. You can pay off the balance before the intro period ends to avoid high interest charges.

If you own a home and have enough equity built up, you can use it as collateral for a loan or line of credit. This typically comes with lower interest rates since it’s secured by your property, but that also makes it riskier.

This option lets you borrow from your own retirement savings and pay yourself back over time. While it doesn’t require a credit check, it should be approached with caution.

Now, let’s figure out if debt consolidation actually makes sense for your situation.

Recommended: How to Negotiate and Settle Your Own Debt

Here’s a quick checklist to help you weigh the pros and cons before jumping in. Your financial habits, credit score, and ability to commit to a plan all play a role in how well this strategy will work.

You might benefit from debt consolidation if:

If you’re still unsure, let’s break down the pros and cons to help you decide if debt consolidation is the right move.

You can also go through our blog, Tips on Debt Relief Scams and Legitimacy.

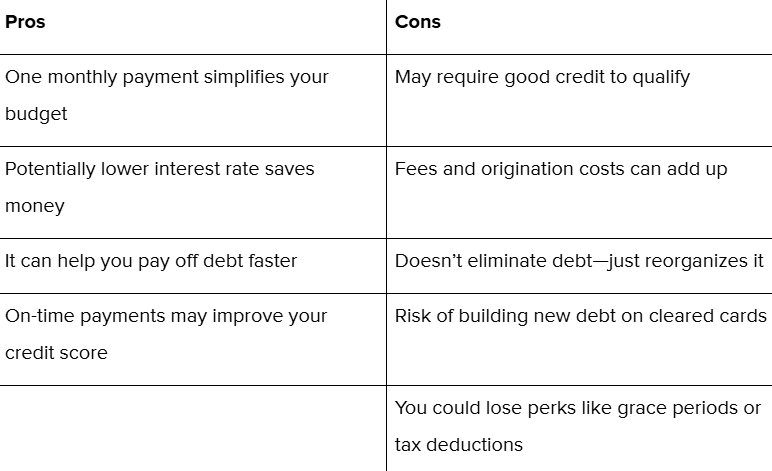

Before you apply for a loan or transfer your balances, it's important to weigh the pros and cons of debt consolidation loans. While this strategy can simplify your finances and reduce interest, it’s not without risks. Here’s a clear comparison to help you decide if it’s worth it for your situation:

Remember, the real benefit depends on how you use this strategy. Consolidation can be a solid step toward financial stability if you're committed to staying on track and not adding more debt.

Also, check our blog, Steps to Establish and Build Credit from Scratch.

Debt consolidation isn’t the only path to becoming debt-free—here are some alternatives worth considering.

Before committing to debt consolidation, it’s smart to understand other options that could offer similar relief, especially if your credit score or financial situation makes consolidation tough. Here’s a quick overview of common alternatives:

A DMP is a structured repayment plan set up through a nonprofit credit counseling agency. You make one monthly payment to the agency, and they pay your creditors, often negotiating lower interest rates or fees. It won’t reduce your balance, but it can simplify payments without taking on a new loan.

This option involves negotiating with creditors to pay less than what you owe. It’s often used when you’re significantly behind on payments. While it can reduce your debt burden, it typically damages your credit score and may involve fees or tax consequences.

If you’re overwhelmed with debt and can’t see a way out, bankruptcy may be a last resort. It can eliminate or restructure debts through legal channels, but the impact on your credit is severe and long-lasting. Always seek legal or financial advice before considering this step.

If you're married, you can also check this option: Joint Debt Consolidation Loans for Married Couples.

Debt consolidation can be a smart move if:

To get a clear idea, you might want to check our blog: Signs You Are In Too Much Debt and How To Get Out.

If you’re not sure whether debt consolidation is right for you, it’s a good idea to speak with a financial advisor or a debt management company like Shepherd Outsourcing. Shepherd Outsourcing can help you assess your situation and determine the best path forward. Shepherd Outsourcing provides step-by-step guidance, from evaluating the best consolidation options to helping you apply for new loans or credit cards.

If you're trying to decide whether debt consolidation is a good idea, the answer depends on your financial situation. For many, it can be a practical way to simplify payments, lower interest, and regain control. But before moving forward, it's important to assess your credit, spending habits, and ability to stick to a repayment plan.

Consider professional guidance if you're feeling overwhelmed or unsure of what to do next. Shepherd Outsourcing Services helps reduce stress by negotiating with creditors, lowering your total debt, and offering customized management plans. They also provide financial counseling and ensure everything stays legally compliant, so you don’t have to handle it alone.

Debt can feel isolating, but support is available. The sooner you take the next step, the sooner you can start building a more stable financial future.

©2024 by Shepherd Outsourcing.